Most Stamp Duty overpayments are not random accidents but predictable consequences of a flawed, high-volume conveyancing system that relies on basic software.

- Solicitors often miss dozens of complex reliefs because standard calculators are not designed for non-standard property transactions.

- Strict, non-negotiable deadlines separate a simple online amendment from a complex, multi-year overpayment claim.

Recommendation: Do not assume your original calculation was correct. The key to recovery is to identify the specific procedural pathway—either a 12-month amendment or a 4-year overpayment relief claim—that applies to your situation.

Discovering you may have overpaid thousands of pounds in Stamp Duty Land Tax (SDLT) is a deeply frustrating experience. You placed your trust in a professional conveyancer, signed the paperwork, and assumed the figure calculated was definitive. Yet, months or even years later, you learn of a missed relief or a calculation error that has cost you dearly. The common wisdom is that SDLT is complex, and while true, this statement often masks a more uncomfortable reality about the property transaction process in England.

Most people believe their solicitor is a tax expert. In reality, their primary role is conveyancing—the legal transfer of property. Specialist tax advice, especially concerning the labyrinthine rules of SDLT, often falls outside the scope of a standard, fixed-fee service. This gap between client expectation and service reality is where costly errors are born. These are not typically individual failings but systemic blindspots, driven by a reliance on basic HMRC calculators that are, by HMRC’s own admission, merely a guide.

But what if the key to reclaiming your money wasn’t just about spotting the mistake? What if it was about understanding the distinct procedural pathways available for correction? This is not a matter of simply asking for money back. It involves navigating a specific set of rules, deadlines, and evidence requirements that differ dramatically depending on when the error is discovered. One route is a straightforward amendment; another is a formal overpayment claim that requires a higher burden of proof.

This guide will illuminate the systemic reasons your solicitor may have miscalculated your SDLT. We will provide a clear, step-by-step process for submitting a correction, analyse the critical choice between using a reclaim agent and dealing directly with HMRC, and dissect the unforgiving deadlines that can render a valid claim worthless. By understanding the system that created the error, you can effectively navigate it to reclaim what is rightfully yours.

This article provides a comprehensive overview of the SDLT reclaim process, from identifying common errors to navigating the official channels for recovery. The following sections will guide you through each critical stage.

Summary: Your Guide to Correcting Stamp Duty Errors

- Why Did Your Solicitor Miss the £2,500 First-Time Buyer Relief You Were Entitled To?

- How to Submit a Corrected SDLT Return Within 12 Months of Your Original Filing?

- Tax Reclaim Agent or Direct HMRC Submission: Which Recovers Overpaid SDLT More Reliably?

- The Valid £8,000 SDLT Overpayment Claim Rejected Because It Was Filed 13 Months Late

- When to Audit Your Historical SDLT Payments: Before Adding Properties or During Annual Tax Planning?

- Why Does Your £1M Property Cost £150,000 in Taxes Before You Even Sell It?

- The 3-Year Deadline That Costs Sellers £20,000 in Unreclaimable Stamp Duty

- How to Save £15,000 on Stamp Duty When Buying Your Second Property in England?

Why Did Your Solicitor Miss the £2,500 First-Time Buyer Relief You Were Entitled To?

The most common reason for a missed relief is not negligence, but a systemic blindspot within the high-volume, low-fee conveyancing model. Many solicitors rely heavily on HMRC’s standard online SDLT calculator to determine the tax due. However, this tool is designed for simple, straightforward transactions and cannot account for the nuances of more complex situations. The scale of this issue is vast; HMRC repaid approximately £1.2 billion in SDLT overpayments during the 2023-24 financial year, a testament to how frequently initial calculations are wrong.

A solicitor’s primary ‘duty of care’ is the successful legal transfer of the property title, not providing in-depth, specialist tax advisory. In a fixed-fee environment, there is often little time or incentive to dig deeper into a client’s circumstances to uncover potential reliefs beyond the most obvious ones. This is particularly true for situations involving mixed-use properties, multiple dwellings, or non-standard buyer circumstances, such as property ownership abroad.

Case Study: The Systemic Flaw in Standard Conveyancing

According to an analysis by SDLT Refunds, a division of Cornerstone Tax, there are over 50 reliefs and exemptions available under Stamp Duty legislation. Many of these are routinely missed by conveyancers who depend on HMRC’s basic calculator, which HMRC itself describes as ‘merely a guide’. This reliance is a systemic issue in the conveyancing industry, leading to widespread overpayments. Interviews with specialists in publications like Forbes and the Financial Times reveal the average overpayment currently stands at a staggering £27,000, underscoring the financial impact of this procedural gap.

Therefore, your solicitor didn’t necessarily make a one-off ‘mistake’. It is more likely the standard process they followed was fundamentally ill-equipped to identify your eligibility for a specific relief. The system is geared for speed and volume, not for the forensic financial scrutiny required to ensure every client pays the absolute minimum, correct amount of tax.

How to Submit a Corrected SDLT Return Within 12 Months of Your Original Filing?

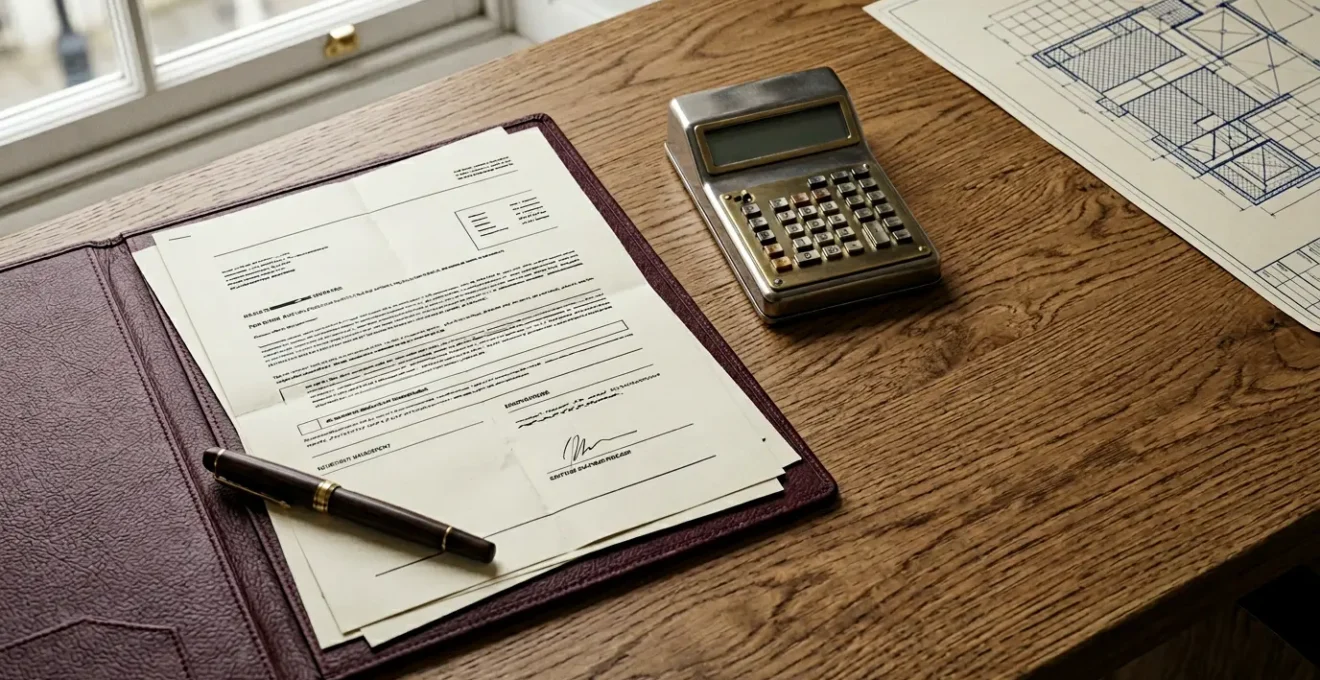

If you identify an overpayment within 12 months of your original filing date, you are in the strongest position. During this window, you have a statutory right to amend your SDLT return. The process is relatively straightforward and can be done directly through the HMRC online portal, without needing to make a more complex ‘overpayment relief’ claim. The key to a successful amendment is meticulous preparation and assembling a « bulletproof » evidence pack before you begin the submission.

The goal is to present a clear, factual case to HMRC that leaves no room for ambiguity. You are not making an argument; you are correcting an administrative error. This requires gathering all relevant documents from your property purchase and presenting them in a logical order. The process should feel less like a dispute and more like a simple correction of the record, supported by undeniable proof.

As the image suggests, precision and attention to detail are paramount. Your submission should anticipate any questions an HMRC officer might have and provide the answers upfront. A well-organised evidence pack not only strengthens your claim but also significantly speeds up the review process, leading to a faster refund.

Your Action Plan: Assembling the Evidence for an SDLT Amendment

- Collect Original Documents: Gather your original SDLT return (the SDLT1 form) that was submitted upon purchase and the completion statement from your solicitor.

- Gather Proof of Payment: Locate the bank statement or section of the completion statement that explicitly shows the incorrect SDLT amount being paid to HMRC.

- Compile Supporting Evidence: Collect all documentation that proves your eligibility for the missed relief. This could be proof of sale of a previous residence for Main Dwelling Relief, or architectural plans and utility bills for a Multiple Dwellings claim.

- Draft a Factual Narrative: Write a clear, concise cover letter. Use neutral, factual language to explain the error (e.g., « The initial return did not account for the property’s mixed-use status »). Avoid blaming your solicitor; focus on correcting the facts of the transaction.

- Submit via HMRC Portal: With your complete evidence pack scanned and ready, log in to HMRC’s online service to formally submit the amendment to your SDLT1 return.

Tax Reclaim Agent or Direct HMRC Submission: Which Recovers Overpaid SDLT More Reliably?

Once you’ve identified a potential overpayment, a critical decision awaits: should you handle the claim yourself directly with HMRC, or engage a specialist tax reclaim agent? For simple amendments within the 12-month window, such as a missed First-Time Buyer’s Relief, a direct submission can be effective if you are organised and confident. However, for more complex cases or claims outside the 12-month window, the expertise of a specialist can be invaluable.

Reclaim agents live and breathe SDLT legislation. They understand the nuances of what makes a claim successful and are adept at navigating HMRC’s internal processes. They conduct a forensic review of your entire transaction, often uncovering additional grounds for a refund that you may have missed. Their experience is reflected in their results; specialist firms report success rates as high as 96% in recovering overpaid tax for their clients. This level of success comes from their ability to build a robust, evidence-based case that pre-empts HMRC’s potential challenges.

The downside is the cost. Most agents work on a ‘no-win, no-fee’ basis, taking a percentage of the refund recovered, typically between 15% and 30%. While this may seem high, it must be weighed against the risk of a DIY claim being rejected due to a poorly constructed argument or missed legal detail, resulting in a 100% loss. Vetting a potential agent is therefore crucial to ensure you are partnering with a credible, regulated professional.

Before engaging any firm, it’s essential to ask the right questions to verify their credentials and understand their process. A reputable agent will be transparent about their fees, professional standing, and how they will manage your case.

- ‘Are you a member of a professional body such as CIOT (Chartered Institute of Taxation), ATT (Association of Taxation Technicians), or RICS (Royal Institution of Chartered Surveyors)?’

- ‘Is your fee structure contingent on a successful reclaim, and what is your exact percentage or fixed fee?’

- ‘Can you provide evidence of your Professional Indemnity Insurance coverage?’

- ‘Who will be my direct contact at your firm if HMRC queries the claim?’

- ‘Will you conduct a full forensic review of my transaction to identify additional overpayments beyond what I’ve identified?’

The Valid £8,000 SDLT Overpayment Claim Rejected Because It Was Filed 13 Months Late

Time is the most unforgiving element in any tax reclaim. The story of the £8,000 claim rejected for being just one month late is a harsh but vital lesson in what specialists call statutory finality. While you have 12 months to easily amend your return online, missing this window does not mean all is lost. However, it does mean you enter a different, more complex procedural pathway: the ‘overpayment relief’ claim. This route has its own strict deadline, which is generally 4 years from the effective date of the transaction, as stipulated under Schedule 10 of the Finance Act 2003.

The critical distinction is the burden of proof. An ‘amendment’ within 12 months is a right. An ‘overpayment relief’ claim is a request that must be justified, often by demonstrating an error of law rather than just a simple oversight. More importantly, these deadlines are absolute. Tax tribunals have consistently shown they have no power to grant extensions, regardless of the circumstances.

Case Study: The Unbending Nature of Statutory Deadlines

The tribunal case of Bredin v Revenue Scotland provides a stark warning. A taxpayer paid the Scottish equivalent of the higher rate surcharge, intending to sell their previous home within the 18-month window. The sale completed just 13 days after the deadline. Despite arguing unfairness due to market conditions, the refund was refused. The Tribunal upheld the decision, stating it had no authority to override clear statutory time limits. As reported by KPMG, this case confirms that tribunals cannot assist taxpayers who miss deadlines, no matter how compelling their reasons.

This precedent underscores a crucial point: the reason for the delay is irrelevant. Whether it’s a market downturn, a slow solicitor, or personal circumstances, once the statutory deadline has passed, the door to that reclaim route is permanently closed. This is why understanding the different time limits and reclaim routes is not just important—it’s fundamental to recovering your money.

| Reclaim Route | Time Limit | Legal Basis | Burden of Proof | Best Used For |

|---|---|---|---|---|

| 12-Month Amendment (Schedule 10 para 6) | 12 months from filing date | Statutory right to amend return | Standard – HMRC may still enquire | Clear errors, missed reliefs, data entry mistakes |

| 4-Year Overpayment Relief (Schedule 10 para 34) | 4 years from effective date | Overpayment relief claim | Higher – must prove error of law, not just missed claim | Complex cases, errors of law, claims outside 12-month window |

| Professional Negligence Route | 6 years from transaction (civil claim) | Claim against solicitor’s PI insurance | Highest – must prove breach of duty and loss | When HMRC reclaim window has closed entirely |

When to Audit Your Historical SDLT Payments: Before Adding Properties or During Annual Tax Planning?

The best time to audit a past SDLT payment is now. The common trigger for a review is often the purchase of a new property, as it brings tax considerations to the forefront. However, waiting for the next transaction is a passive approach that risks running down the clock on crucial reclaim deadlines. A more proactive strategy is to incorporate a historical SDLT review into your annual tax planning, alongside checking your income tax, capital gains, and inheritance tax positions.

By treating SDLT as a dynamic part of your financial health, you shift from a reactive to a proactive mindset. The 4-year window for overpayment claims may seem long, but it evaporates quickly. An annual review ensures you never miss an opportunity to correct a past error. The first step in any audit is organisation. If your documents are scattered across emails and folders from years ago, the task can feel overwhelming. The key is to create a ‘digital shoebox’ for each property transaction you have ever made.

This centralised, organised archive not only makes a future audit straightforward for you or a specialist but also serves as an invaluable record for future capital gains calculations when you eventually sell the property. Setting up this system for past transactions and maintaining it for future ones is one of the most powerful and simple steps you can take to protect yourself from overpaying tax.

Creating your digital archive is a methodical process:

- Create a Digital Folder: For each property, create a dedicated folder labeled with the address and completion date.

- Scan Core Documents: Scan and save the original SDLT1 return and the SDLT5 certificate (the confirmation of filing) issued by HMRC.

- Save Financials: Archive the final completion statement from your solicitor, which details all financial aspects of the purchase.

- Store Correspondence: Save all emails and letters with your solicitor, especially any discussions regarding the SDLT calculation or potential reliefs.

- Keep Property-Specific Evidence: Store valuations, surveys, and evidence related to the property’s condition or use at the time of purchase (e.g., photos of a derelict state, proof of mixed-use).

- Set Calendar Reminders: Proactively set alerts at key intervals: 11 months post-filing (amendment deadline), 3 years post-purchase (higher rate refund deadline), and 3.5 years post-purchase (final overpayment window warning).

Why Does Your £1M Property Cost £150,000 in Taxes Before You Even Sell It?

The initial purchase price of a property is only the beginning of its true cost. The tax burden on UK property, particularly in England, is multi-layered and cumulative, starting with a significant upfront hit from Stamp Duty Land Tax. For a £1 million property, the tax can be substantial, but it’s the various surcharges and tiered rates that cause the figure to escalate dramatically, often reaching into the six figures before you’ve even spent a night in the home.

The single biggest inflator of an SDLT bill is the higher rate for additional dwellings. If the property you are buying is not your only property worldwide and you are not replacing your main residence, you are subject to this surcharge. This additional tax isn’t just applied to a portion of the price; it’s a flat percentage on the entire purchase value, levied on top of the standard residential rates. This surcharge was recently increased, further amplifying the tax cost of property ownership for investors and second-home buyers.

As the visual of a classic English property suggests, ownership is a long-term financial commitment with tax implications at every stage. The initial SDLT payment is just the entry ticket. Beyond this, you face ongoing Council Tax, potential Capital Gains Tax (CGT) upon sale, and ultimately, Inheritance Tax (IHT) when the asset is passed on. The £150,000 figure on a £1M property becomes plausible when you factor in a higher rate SDLT charge, which includes the standard rate (£38,750 as of late 2024) plus an additional surcharge on the full purchase price. For example, a 5% surcharge would add another £50,000, bringing the total closer to £90,000—and this is before other transaction costs are even considered. Any error in applying reliefs could push this figure even higher.

The complexity doesn’t end there. The interaction between different taxes can be a minefield. For instance, the SDLT you pay is not deductible from your capital gain when you sell, meaning you are taxed on the acquisition and again on the growth in value. This layering of taxes is precisely why ensuring your initial SDLT calculation is correct is so critical—overpaying at the start only exacerbates the total lifetime tax cost of the property.

The 3-Year Deadline That Costs Sellers £20,000 in Unreclaimable Stamp Duty

One of the most common—and painful—scenarios for overpaying SDLT involves the ‘replacement of main residence’ rules. When you buy a new main home before selling your previous one, you are forced to pay the higher rate of SDLT upfront. However, HMRC allows you to reclaim the surcharge element if you sell your previous main residence within three years. This three-year window sounds generous, but in a slow or unpredictable property market, it can become a ticking time bomb that costs homeowners tens of thousands of pounds.

The deadline is not for accepting an offer; it is for the legal completion of the sale. This is a crucial distinction. A sale can easily be delayed by weeks or months due to buyer issues, survey problems, or legal chain collapses. As we’ve seen, HMRC and the tax tribunals enforce these deadlines with absolute rigidity. Selling your previous home just one day after the three-year anniversary means your right to a refund is extinguished forever. This creates immense pressure on sellers as the deadline approaches.

Case Study: Reclaiming the Higher Rate Surcharge

Consider a couple who bought a new home for £600,000 while still owning their previous one. They paid the higher rate SDLT, including the additional surcharge. Two years later, they sold their previous residence. As detailed in a guide by the estate agent Hamptons, because this sale occurred within the stipulated three-year period, they became eligible to reclaim the surcharge. In this example, the refund amounted to £30,000. Crucially, the claim for this refund must be made within 12 months of selling the previous residence, adding another layer of time sensitivity to the process.

In a challenging market, sellers approaching their deadline face a difficult choice: hold out for their desired price and risk losing the entire SDLT refund, or accept a lower offer to guarantee the sale completes in time. Proactive management is the only way to navigate this high-stakes countdown.

- 30-Month Review: Get a realistic, up-to-date valuation of your property to understand its current market position.

- Pricing Strategy: Discuss with your agent whether a price reduction is a sensible investment to secure the much larger SDLT refund.

- Document Everything: Keep a detailed record of all marketing efforts, viewings, and offers. This can provide evidence of your reasonable attempts to sell if you narrowly miss the deadline.

- 33-Month Consultation: Speak to a solicitor about the very limited grounds for an ‘exceptional circumstances’ extension, such as public authority restrictions preventing the sale.

- Calculate Break-Even Point: Determine the maximum price cut you can accept where the financial benefit of securing the SDLT refund still outweighs the reduction in sale price.

Key takeaways

- Systemic Flaws, Not Isolated Errors: Most SDLT overpayments stem from the standard conveyancing process’s reliance on basic calculators, which are not equipped to handle complex reliefs.

- The Two Procedural Pathways: Your reclaim route depends entirely on timing. You have a right to amend your return within 12 months, but after that, you must make a more complex ‘overpayment relief’ claim within 4 years.

- Deadlines Are Absolute: Tax law is unforgiving. Whether it’s the 12-month, 3-year, or 4-year window, missing a deadline by a single day will almost certainly render your claim void, regardless of the reason.

How to Save £15,000 on Stamp Duty When Buying Your Second Property in England?

Saving a significant amount on a second property purchase often comes down to identifying reliefs that fall outside the scope of a standard conveyancing check. While the higher rate surcharge is a major hurdle, specific circumstances of the property itself can unlock substantial savings. One of the most prominent historical examples was Multiple Dwellings Relief (MDR), which, until its abolition for transactions from 1st June 2024, was a frequent source of successful reclaims.

MDR allowed buyers of properties containing more than one ‘dwelling’ (e.g., a main house with a self-contained ‘granny annexe’) to calculate SDLT based on the average price of each dwelling, rather than the total. This allowed for multiple uses of the lower tax bands, often resulting in huge savings. Although MDR is no longer available for new purchases, claims for transactions that completed before June 2024 can still be made within the statutory time limits. This makes it a prime target for a forensic audit of historical property purchases.

Case Study: Multiple Dwellings Relief for a Granny Annexe

A client of SCA Tax purchased a property in May 2022 that included a self-contained granny flat. The original solicitor calculated SDLT based on a single dwelling. SCA Tax successfully argued for Multiple Dwellings Relief, as the annexe had its own kitchen, bathroom, and entrance. This approach, which calculated the tax based on the average value of each dwelling, secured an SDLT refund of £5,600 for the client. This case highlights how specialist knowledge can unlock reliefs missed during the initial transaction, and remains relevant for historical claims made within the 4-year overpayment window.

However, claiming such reliefs is not without risk. HMRC has become increasingly stringent in its interpretation of what constitutes a ‘separate dwelling’. A simple annexe is not enough; it must have privacy, self-sufficiency, and independent access. Indeed, the Chartered Institute of Taxation (CIOT) noted that in a sample review, HMRC considered 40% of MDR claims to be contentious or incorrect. This highlights the tightrope you walk: the potential for significant savings is real, but a poorly evidenced claim is likely to be rejected. The same principle applies to other complex reliefs, such as those for mixed-use properties or uninhabitable dwellings, where expert assessment is crucial.

The logical next step is to move from awareness to action. A professional, no-obligation audit of your past property transactions is the only way to know for sure if you are one of the thousands who have overpaid. By having a specialist review your case, you can gain clarity and begin the process of reclaiming what is rightfully yours.